SPARX Japan Asia Focus Strategy Japan Asia Focus Growth Strategy: Performance Review 2024

Portfolio Manager, SPARX Japan Asia Focus Strategy

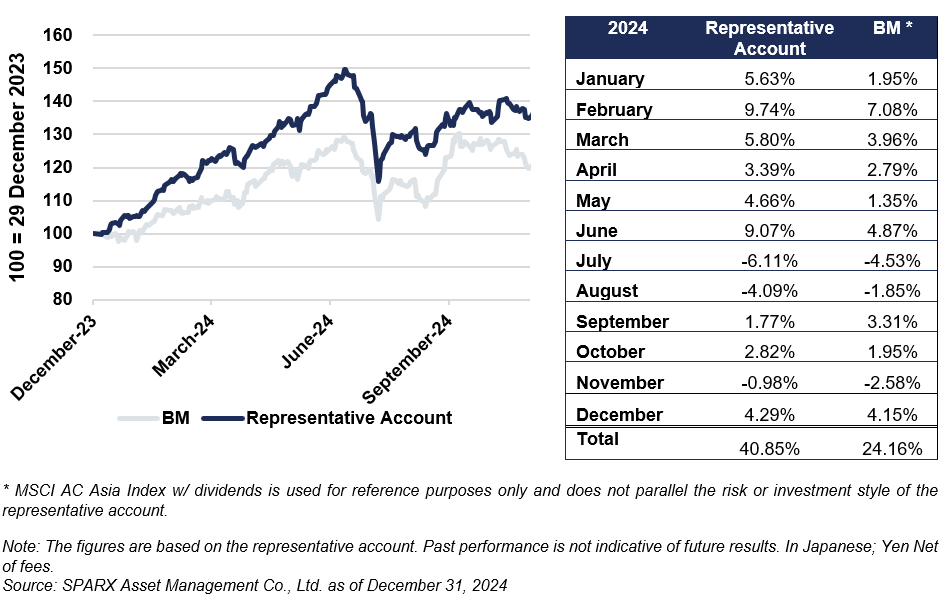

2024 was a year full of surprises and volatility in Asia. Fortunately, the strategy achieved a relatively good performance.

As we close the year, I would like to provide some thoughts about what we saw in Asia in 2024 regarding our strategy. At SPARX, we are bottom-up investors, and the key attractiveness of Asia is the large and diverse opportunity sets. While we are aware of the macro environment, macro is not where we concentrate our time and resources on. Instead, we focus on studying and meeting companies. Therefore, what we are going to write is not focused on GDP growth, inflation, currency, etc. but something more micro such as trends in certain industries, especially those related to our strategy.

As Asia is too broad, I will mainly focus on 1 thing for each market. This is what our strategy does. We do not own many things but only 25-35 holdings across the whole region. This concentrated approach allows us to simply focus on the most attractive few things in each market to build the portfolio.

Japan - corporate governance reform

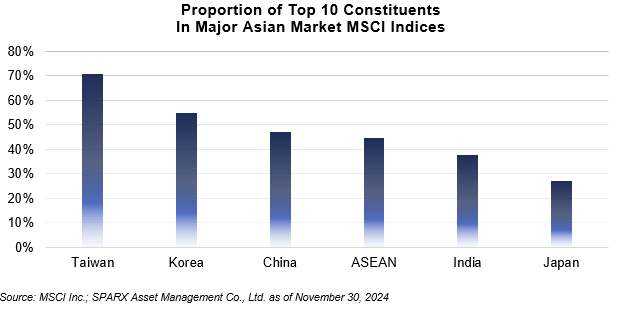

Japan was the largest contributor of absolute return for the strategy in 2024. When people asked for my view on Japanese stock market, I say Japan is a very diverse market and it is hard to conclude a market driver easily, although Yen movement does have its influence (and my colleague has written about it here). If we take a look at the MSCI Indices, we can see what I mean by saying Japan is diverse. For example, in MSCI China Index, the top 10 constituents account for over 45% of the index weight, and all of these are either internet or financial companies. Such a skew to certain sectors and concentration in the top companies can also be seen in Taiwan, Korea and ASEAN, while India is more diverse. For Japan, the top 10 constituents only account for approx. 27% of MSCI Japan Index, and they spread across a number of industries. Because of this, I am reluctant to give a broad picture of the Japanese markets.

If I need to write one thing, as I already wrote about IP businesses in my last commentary, I will pick corporate governance reform. My colleague have written extensively about this topic here, so I am not adding more on that. Importantly, corporate governance reform is not an empty slogan but has real impacts to stock performance. One of the sectors that generated decent returns was the Japanese non-life insurers in 2024.

Japanese non-life insurers are large holders of so-called policy-shareholdings that are worth trillions of Japanese Yen. The insurers purchased these shares (hundreds of stocks of public companies such as Toyota Motor) in the 1960s for building and maintaining business relationships in corporate insurance. After decades of holding the stocks, huge amount of unrealized gains have piled up. However, these holdings have been "under-utilized asset" for a long time and represent a kind of inefficient capital management. In early 2024, the Financial Services Agency of Japan (FSA) requested that insurance companies accelerate the sale of policy-shareholdings as part of their business improvement plans, with a submission deadline of February 2024. In response, each company expressed committement to selling off all such shares over the next 6-7 years. The release was well-received by the market. As a result, stock prices surged significantly in 2024. This is one example how investors can profit from the improvement of corporate governance and capital efficiency of Japanese companies.

My peers often ask "Where is the upside of Japan? There is no EPS (earnings per share) growth if Yen does not depreciate!". It is a common impression that there is no EPS growth in Japan as the country has had minimal economic growth for more than 30 years. As I wrote above, I belive that Japan is very diverse and there are lots of very good individual companies (such as Sanrio that I wrote the October 2024 commentary) who can grow EPS at a decent pace. On the other hand, corporate governance reform can become an important driver. 1 common example is improved shareholder returns in the form of share buybacks. If shares are bought at a low valuation, which is often the case in Japan, the buyback itself can drive EPS growth.

On organic growth, many large Japanese companies possess excellent technologies or manufacturing capabilities that could set them up well to capture the global growth of semiconductor, energy transition, healthcare, etc. However, many companies have diversified business lines, many of which are segments with low profitability. If companies started to emphasize capital efficiency, they would start to get rid of those inefficient units and recycle the capital to invest in areas where they have strengths and with attractive growth prospects. This will drive the organic growth of these companies. Also, by reducing the inefficient complexity, it can make the attractive parts of the business more visible to outside investors. Because of that, the strategy has invested in a number of such conglomerates with world class competitiveness in certain areas.

India - consumer discretionary is taking off

India was the 2nd largest contributor of absolute returns in 2024 for this Strategy. It is not difficult to see India as a fast growing economy with a huge, young and educated population, which presents very attractive opportunity sets in the consumer sector. When investors think of Indian consumer companies, they often think of consumer staples such as Hindustan Unilever or Nestle India. Indeed, these companies that fulfil the basic consumer needs have generated significant returns to investors in the past 2 decades. However, our preference is in consumer discretionary service. There are 2 reasons:

- I believe the country is ready for a significant acceleration in discretionary spending. GDP per capita of US$2,000 is usually seen as an inflection point. China crossed that in 2006 and India crossed that in 2019 for the first time.

- In investing in consumer sector, my preference is categories with high spending ceiling, meaning categories in which people will keep spending ever more money when they get richer and richer. I will write about instant noodle later, but instant noodle is a category with an obvious ceiling. One will not keep spending more on instant noodle after a certain level. Likewise, I generally prefer service than goods. Some of my preferred consumer categories across the region include: entertainment, travel, beauty, convenience (when we get richer, we often spend money to buy time), etc.

The room in India consumer discretionary space is huge. Take hotel as an example, one of my holdings is the largest listed hotel company in India, The Indian Hotels Company (IHCL). As of 3Q2024, it managed roughly 25,000 rooms. Another large listed hotel company, Lemon Tree Hotels, managed roughly 10,000 rooms.Comparing that to China, H-World (one of leading hotel companies in China) managed about 1 million rooms in China in 3Q2024 and the number is still growing. We invest in a number of these consumer discretionary service companies, notably in travel and convenience segments. And they were very good returns contributors in the past 2 years.

Looking forward, I am cautious about the high near-term valuation of many Indian stocks, especially those in the small and mid cap space. On the other hand, there are reasons to believe India should deserve a considerable premium. In many Indian companies we studied, they are among the most conscious of returns on capital in the region. Many companies have decades, if not more than a century, of history surviving through crisis and are run by management who take a long-term view. IHCL's key hotel brand Taj opened its first hotel in 1903 and IHCL's parent Tata Group was founded in 1868. The country is fast growing with young and educated population. I maintain an optimistic view but take a conservative stance when picking stocks in India.

Korea - K-wave continued

Korea was the worst performing market in Asia in 2024. Yet, it was the 3rd largest contributor in 2024. While the market performance was weak, the Strategy only holds around 2-4 stocks in Korea most of the time. If it is right about holding these 2-4 stocks, it could make it possible to record positive performance even in the weak market enviroment. The same can be said about other markets.

People usually think of semiconductor and Samsung when they think of Korea. This is not where I focus on. I sold our holdings in Samsung Electronics middle of the year and avoided the subsequent drawdown. In my view, there are other things in Korea much more interesting than semiconductor. As I wrote in the October 2024 commentary, thhis Strategy once made a decent profit from K-pop companies. K-wave is more than K-pop: There are K-beauty, K-food, K-drama, etc.

One of the biggest contributors in 2024 was an instant noodle company called Samyang Foods. It sells a very spicy, fried (non-soup) type of instant noodle called Buldak (meaning "Fire Chicken" in Korean). Its original flavor is very popular in Asia. However, the flavor is probably too spicy for the rest of the world. Then, it launched a less spicy carbonara-flavored noodle. It was reportedly inspired by observing netizens who added cream and cheese to the original flavor noodle to make it less spicy. The carbonara noodle became a global hit, partially helped by social media such as TikTok. Believing the carbonara noodle can better fit the taste of the global market and observing improving growth momentum, we invested in the company.

Looking forward, Korea is the market we are less optimistic about given the risk of trade tariff. Within the region, Korea has one of the highest US exports exposure and many companies will need to compete with US local manufacturing. Take Hyundai Motor as an example, less than 40% of its US sales volume are locally produced, with the rest relying on imports from Korea.

Another point to note is Korea is the "Value Up program", which tries to learn from Japan's TSE reform to improve shareholder returns. We did see some sectors such as banks actively communicating with the markets about improving shareholder returns. We invested in a Korean bank and have already taken profit after sharp rise in share price. However, we still saw many companies resistant to change, especially the Chaebols. There were some restructuring with the Chaebol affiliated companies in 2024, some of which still aim at benefitting the major shareholder at the expense of the others. On the other hand, many companies announced the "value-up" program, quite a lot of them are underwhelming. We believe this is due to, at least partially, challenging environment either from the macro or competition from elsewhere such as China. The challenge in Korea is about the fundamentals. If fundamentals is weak, there is not much value left for shareholder returns.

Taiwan - all about AI

Similar to Korea, people usually think of semiconductor when they think of Taiwan. Taiwan is the market I travelled to most in 2024. Aside from TSMC, Taiwan has an amazing ecosystem of semiconductor supply chain from design to manufacturing. What amazes me is there are many articles and YouTube videos in Taiwan that explain the complicated technology in layman terms. As the CEO of AMD Lisa Su noted: "Taiwan is probably the only place in the world where everybody knows what CoWoS is without explanation". Therefore, it is important for us to visit Taiwan regularly to understand the latest trend.

I turned less optimistic about semiconductor in the middle of the year. I believe AI semiconductor will continue to grow as the US hyperscalers is expected to continue to increase capex in 2025 and 2026, but the rate of change is likely to go slower and slower. Without a breakthrough in AI applications, a lot of the positives in AI semiconductors are already priced in . We should not forget semiconductor is a highly cyclical industry. Of course, technology is fast moving, and I amd ready to change my view as neccessary.

SE Asia - forgotten but a lot of value

The current global investment landscape is largely shaped by passive investing and ETFs. Usually, this favors the larger markets. When people say they buy US ETF, or Japan ETF, they usually mean the S&P 500 ETF and the TOPIX ETF, which are the large cap stocks. I believe this is one of the reasons why the valuation gap between large and small-mid cap seems to get wider. Within Asia, we may hear people buying the Japan ETF or the India ETF, but we seldom hear anyone buying the ASEAN ETF. As the smallest market in Asia, it is not often the focus.

ASEAN has been a market with a promise that has not been delivered yet. The promise is the rising middle class given the young and large population. However, investors have been disappointed about returns in the region for more than 10 years. The commodity downcycle and strong USD after 2014 were big drags to many ASEAN countries. Then, some of these countries were hit hard by COVID-19 and the subsequent high inflation. Some of these impacts are still lingering. On the bright side, ASEAN is one of the biggest beneficiaries of China + 1. Malaysian market, after recording negative returns (in USD terms) after 10 years, had a strong rally in 2024 thanks to increased investments in semiconductor, data center, etc. into the country. The industry upgrade in the region will be an important driver. Also, I see many well-run ASEAN companies trading at very cheap valuation.

As ASEAN is a forgotten market, we generally do not expect anyone will come to re-rate the stocks there, even though they are cheap. We need to invest in companies that we can get paid by the companies themselves through dividend. The Strategy is holding a company listed in Hong Kong called First Pacific. First Pacific is owned by Anthony Salim, one of the richest men in Indonesia. The company mainly owns Indofood, the largest instant noodle company in the world, and a range of important infrastructure assets including utilities, toll roads, telecom operator, in the Philippines and Indonesia. Currently, it pays a dividend yield of higher than 5% and the company commits to a growing dividend. In addition, it is growing the portfolio of stable assets in ASEAN. We believe it is attractive. Interestingly, First Pacific is in the Stock Connect, meaning mainland Chinese investors can also invest in it. The low interest rate in China will continue to drive the market to look for stable, income-generating assets for a long time, I believe it is an attractive asset to those mainland investors who want to get exposed to the fast growing ASEAN economy and a decent dividend income.

I am cautious about the high valuation about certain part of the global markets, especially the US market. Multiples can go up and down with unpredictable market sentiment and it can be illusional sometimes. Under such environment, the low valuation and the high dividend yield in ASEAN seems like the most "real".

China - our biggest mistake of the year

China was probably the biggest surprise in the region. The stimulus measure announced in late September 2024, which helped HK/China becoming one of the better performing markets in the region. Interest rates in China has declined significantly. In fact, China 30-year government bond yield is now lower than that of Japan. I believe the low interest rate driving the market to look for stable, income-generating assets will continue for a long time.

The economic environment remains challenging as China needs continuous and forceful fiscal stimulus to tackle the balance-sheet recession. Tackling balance-sheet recession is a long-term battle, as it took more than 30 years for Japan to get out of it. If the stimulus policy is not persistent enough, the economy will fall back to a deflationary spiral. Market sentiment will remain driven by news around fiscal stimulus policy. Sino-US relations will be another focus. However, I believe many of the bad news around further deterioration of Sino-US relations is already priced in.

My biggest mistake in 2024 is not a mistake of commission but omission. I missed a company that sells "pop toys" whose share price went up by more than 300% in 2024, even though it is a company we certainly understand given our investments in Sanrio. In fact, I visited some of their stores and were impressed by it. I did not invest because the valuation appeared a bit expensive especially compared to the broader HK/China market. This company's IP gained global popularity, partially helped by some high profile celebrities, including global K-pop stars, buying the toys. Instead of calling the products "toys", it would be more accurate to call them collectibles. Similar to gatcha, it has a kind of addictive attractiveness for people to collect the whole set.

As this company has shown, there are companies in China who can find ways to thrive even under a weak environment. Consumer is a highly attractive sector: when economy is good, there are companies that benefit, but it is also true even economy is bad. It is about observing closely consumer behavior and see where their wallet money is going. Fortunately, my strategy also benefitted from some categories that remained resilient, such as travel and quick service restaurants.

Management of many Chinese companies know their stocks are cheap and they are taking steps to address that by stepping up share buybacks or dividend payment. We want to find companies that exhibit resilience under economic weakness and provide a reasonable shareholder returns. China has a huge number of companies. I only own around 25-35 holdings, which mean we probably only need 5 or so good ideas in China. I believe it is a large enough universe for us to find those few ideas.

Conclusion - we are bottom-up investors

We are generally macro-agnostic, but we are prepared to see a lot of volatility in the global market in 2025. The great thing about Asia is it is very broad and diverse. There are companies with world class competitiveness in Japan, Korean, Taiwan. On the other hand, there are great domestic stories like India and ASEAN. We continue to uncover the stocks from the bottom-up and I believe as we stick with our quality and valuation discipline, I can navigate the macro uncertainty.

Important Disclaimer

This content has been prepared by SPARX Asset Management Co., Ltd. (SAM) for information purpose only. Certain information contains economic trends and performance, however, SAM does not warrant the accuracy or completeness of such information, and accept no liability whatsoever for any direct or consequential loss arising from any use of this content. The views and opinions contained herein are based on then-current beliefs of the authors and are subject to change without notice. Furthermore, it should not be assumed that past performance is an indication of future results. Reference to particular securities and their issues are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell securities. Opinions are based on current market conditions and are subject to change without prior notice.